Frederick Peters

President Emeritus

The New York real estate market has been dominated by two phenomena during the second quarter of 2015: absorption of well-priced properties and lack of inventory. The pace of the market picked up in late March after the rather slow first quarter, driven by an improving economy, the end of what seemed at times like an endless winter, and listings both new and reduced. These listings, when their prices met with popular approval, were absorbed easily throughout the marketplace. However, when those prices seem excessive, be it for a one bedroom co-op on First Avenue or a new condominium penthouse downtown asking $30 million, buyers don’t bite. Prices in most segments are neither rising nor falling; our market remains both stable AND ultra value-conscious.

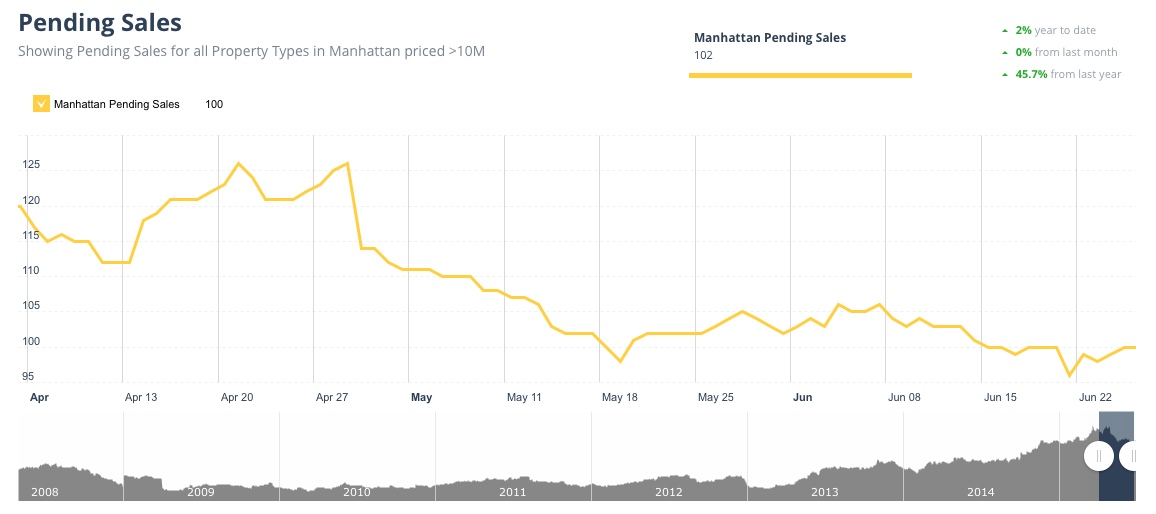

At the very top of the market, the global ultra-rich continue to buy, although more conservatively than they did in 2014. International attention continues to focus on such buildings as 432 Park, which rises like a giant hubristic finger from its perch on 56th Street, and 220 Central Park South, which casts a long shadow both literal and financial over its neighbors and environs. But elsewhere in the city many properties costing upwards of $25 million are languishing on the market; there may simply be more supply than demand in that rarefied arena.

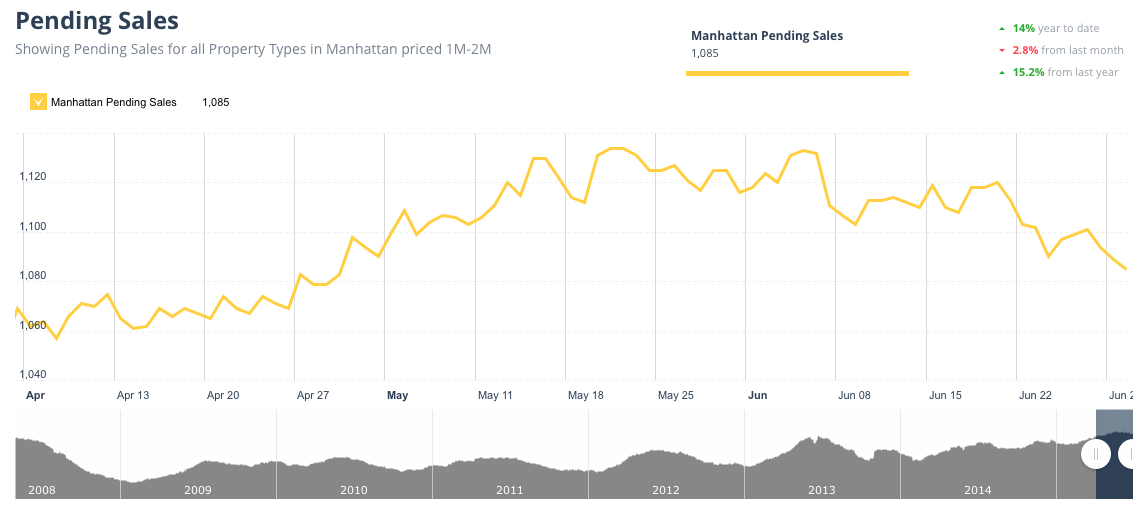

In almost every other segment of the market, however, the issue facing buyers is too little inventory, not too much. Although the market experienced an uptick in inventory as the spring began, anything in good condition with a reasonable price was snapped up immediately. Weekend open house attendance remains at record levels, and multiple offers during the first week on the market drive some prices well above ask, especially in the $2 million and under price range. One phenomenon which is new to me, but which we have seen numerous times in recent months, shows the buyer bidding aggressively to secure a property he is not even certain he wants to buy. Once his offer has been accepted THEN he will weigh the options and decide whether to go forward or not, having won himself a little time to think. As a result, many times the buyer who is second in line will be the one to end up with the property. It’s not unusual for HIM to drop out as well, either because he feels he is overpaying now or because something else has caught his eye.

The biggest issue when winning buyers decide to walk away from a competitive bid deal concerns seller expectations. Even if the winning bidder explicitly states that, after thinking it over, he feels he has offered too much, and the seller now has that high number in his or her head. Even though that buyer was not real, he can become the price benchmark by which all subsequent offers are judged. Such unrealistic expectations can delay the process by which a real, but realistic, buyer for the property can be brought to contract.

Throughout the market in both Brooklyn and Manhattan (and, increasingly, Queens), newer areas continue to heat up. $2 million asking prices are more and more common for brownstones in Bed-Stuy and Long Island City; lofts in Bushwick become costlier (and concurrently less cool) each season. Both new condos and quality conversions in lower West Harlem are selling briskly at over $1,000 per foot, and Washington Heights is flourishing and increasingly in demand. As the city’s population continues to grow, the fingers of the real estate boom reach ever outward and upward.

Each year our market tells a little more of a tale of two cities. The new condominiums priced for tens of millions, much written about by the media, have little to do with the residential choices made by most New Yorkers. Absorption rates for this new super luxury product follow a completely different trajectory from those for co-ops and older condominium units being bought by a professional class which plans to live in them, shopping in local markets and maybe walking their children to nearby schools. These markets move fast, and the residential micro markets diverge more with each passing quarter. As the schism widens, it creates another set of imperatives in the lives of agents: make sure buyers and (especially) sellers understand how their marketing efforts need to be directed, and which statistics apply to their particular property. In 2015, our market behavior has become almost as diverse as the populations we serve.