Frederick Peters

President Emeritus

Two weeks ago, one of our Warburg agents listed a two-bedroom, one-bath prewar co-op apartment, well located in Carnegie Hill, for $999,000. In the first 48 hours, the property was viewed over 1000 times on StreetEasy (which serves as our local MLS), leading to multiple appointments by the middle of the following week. This same agent has several additional exclusives, ranging in price from just under $4 million to just over $10 million. Weeks can go by on these properties without a meaningful appointment.

The above story illustrates better than any other the current state of the Manhattan real estate market. It’s feast or famine, with the feast in the marketplace below $1,500,000 and the famine for properties above $3,000,000. The overall environment remains excruciatingly price sensitive, with holdout sellers seeing no showings for their properties while those who lower to market levels stand a far better chance, although in the current environment there are no guarantees. The question we are often asked: at what price could you sell my home tomorrow? – has become almost impossible to answer. There has been such a fall-off in both demand and urgency, especially in the upper price ranges, that some of the units we see may just not possess real selling potential today.

Our market slows every four years in the lead up to Presidential elections. This year, with its highly polarizing tone, that trend seems exacerbated. Furthermore, the higher reaches of our marketplace in recent years have been driven by groups all of whom have fallen on harder times. We see almost no Russians in the condominium market, and many fewer Chinese. Turbulence in the Eurozone continues to inhibit buyers from Europe, while the Brexit has undermined the economic confidence of wealthy Britishers. The price of oil has slackened demand from the Middle East. At the same time, here at home, hedge fund results have skewed significantly lower during the past 18 months, leaving both their operators and investors with less disposable income than before.

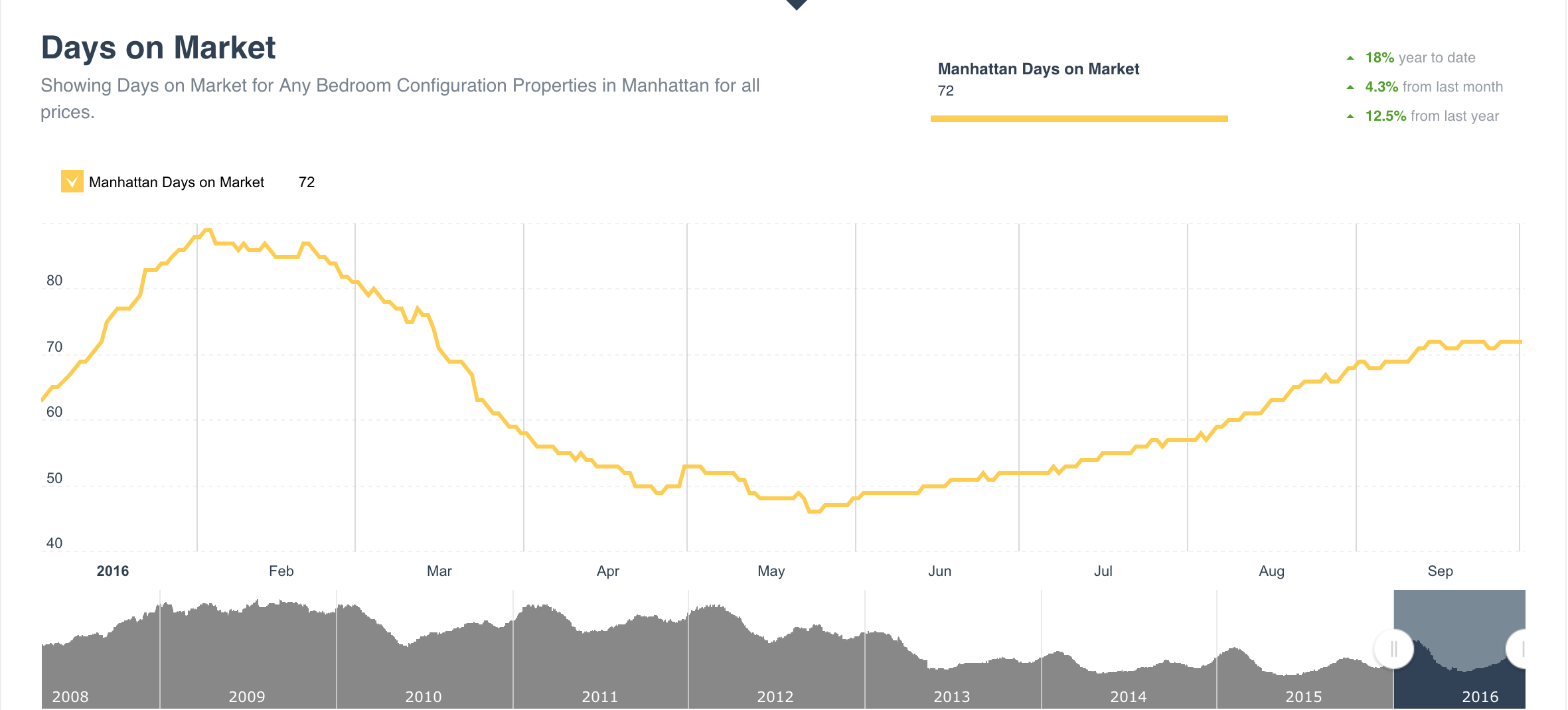

How does this translate into what’s happening on the ground? The pace of sales throughout the marketplace has slowed dramatically over the past quarter. Inventory has increased, and in many property categories, especially high-end condos and larger co-ops needing work, homes are remaining on the market six months, nine months, even a year or more, often with several price cuts, before being sold.

Source: UrbanDigs

Sellers who do not price precisely on point court the danger of being irrelevant in the marketplace. Now more than ever, buyers ignore properties which are priced wrong, although even with accurately priced units today’s buyer may offer 10% below. Sales prices are trending lower than they were six months ago in the higher price categories of both condos and co-ops, with January’s $7 million property being today’s $6.5 million property, and January’s $30 million property being today’s $27 million property. One of New York’s great agents said to me many years ago, “Don’t bother reducing a price less than 10%.” In today’s market, that holds more true than ever.

Because of their lower price points, many of the city’s less established neighborhoods enjoy healthier demand than the Upper East and West Sides and Tribeca. Harlem remains hot, as do parts of the Upper East Side east of Third Avenue, especially in the upper 80s and 90s. Well priced condos suitable for families seem especially popular.

The apartment market throughout Brooklyn continues to draw buyer interest and offers, even as the fancier and more expensive condominiums and townhouses in Williamsburg, Brooklyn Heights and Park Slope can linger now that they are priced more like their Manhattan counterparts. As development and gentrification move deeper into areas like Bushwick, Crown Heights and Prospect Lefferts Gardens, and as more Manhattanites discover the wonderful housing stock in neighborhoods like Ditmas Park and Bay Ridge, the Brooklyn juggernaut appears likely to continue without the encumbrances which are weighing on Manhattan.

The same equation holds true in the rental market: while there is still demand (although an increasing reluctance to pay commissions!) at the lower end of the rental spectrum, tenants have less and less appetite for paying the huge prices for new condo rentals which we saw a couple of years ago. Perhaps that reflects the vast increase in supply as so many investors close on their just-completed units and make them available for rent. Several of our very high-end rentals were forced to accept leases at 20% below what they had received previously in order to keep their properties occupied and income-generating.

To summarize, less expensive units citywide are still in demand, but an inverse graph exists between demand and price: the former shrinks as the latter increases. I don’t foresee any change in this until the end of the year. Depending on the election results, continued strong job growth, and relatively minimal change in mortgage rates in the wake of the now likely year-end increase in the Federal interest rate, we could see a more active and robust market in January. But for now, buyers and tenants have the upper hand.