Frederick Peters

President Emeritus

Download Q3 2019 Market Report

To coin a phrase, all bad things must come to an end. While the New York City real estate market remains challenging, the second quarter brought more activity and more deals than in any of the preceding three quarters. Ongoing price capitulation has driven this uptick more than any other factor; buyers seem willing (and sometimes even eager) to transact as long as they feel they receive value for their money. This has been true throughout the marketplace, from studios and one-bedrooms all the way up to the grandest condos and townhouses. Proper pricing, and curb appeal, rule the day.

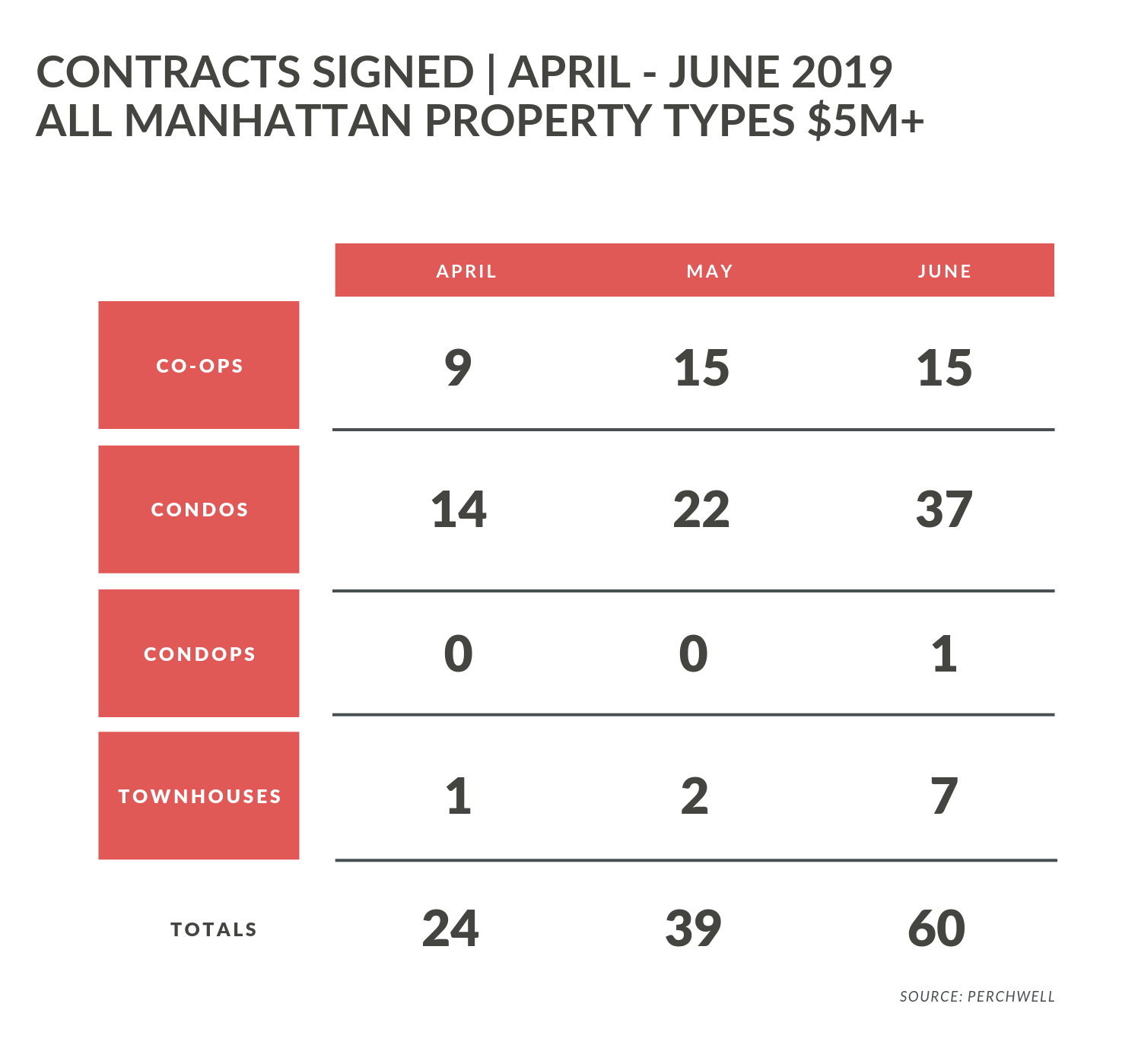

Especially in the upper reaches of the market, at $5 million and over, the change in the mansion tax has also created motivation for buyers and sellers alike. Since after July 1, all deals not signed before April 1 will be burdened by anywhere from 1.5% to 3% in additional tax cost at closing. The push to close in advance of the end of the quarter has been strong. Furthermore, it seems highly probable, especially for prices in excess of $15 million where the difference really becomes meaningful, that the obligation for buyers to pay hundreds of thousands more in mansion tax will impact their decisions about how much to pay for the property they seek. In a buyer’s market such as this one, sellers cannot reasonably expect that buyers will shoulder this burden alone. Sellers will also need to take part of the financial hit.

The feeling buyers have that they are in charge can disappear quickly when a property is priced right. The second quarter saw a substantial increase in competitive bidding for these properties. While competitive bids rarely settle much, if at all, above the asking price, the mere fact that numerous other people are bidding shocks buyers who believed they were the only ones taking advantage of opportunities in the marketplace. Big one-bedrooms in the $700,000’s, any two-bedroom under $1 million and even up to $1.2 million (provided it offers two full bathrooms) — can be almost certain of quick and substantial attention. Those properties, in all price ranges but especially above $10 million, which have lingered for over a year on the market, almost always suffer from too much seller optimism on price.

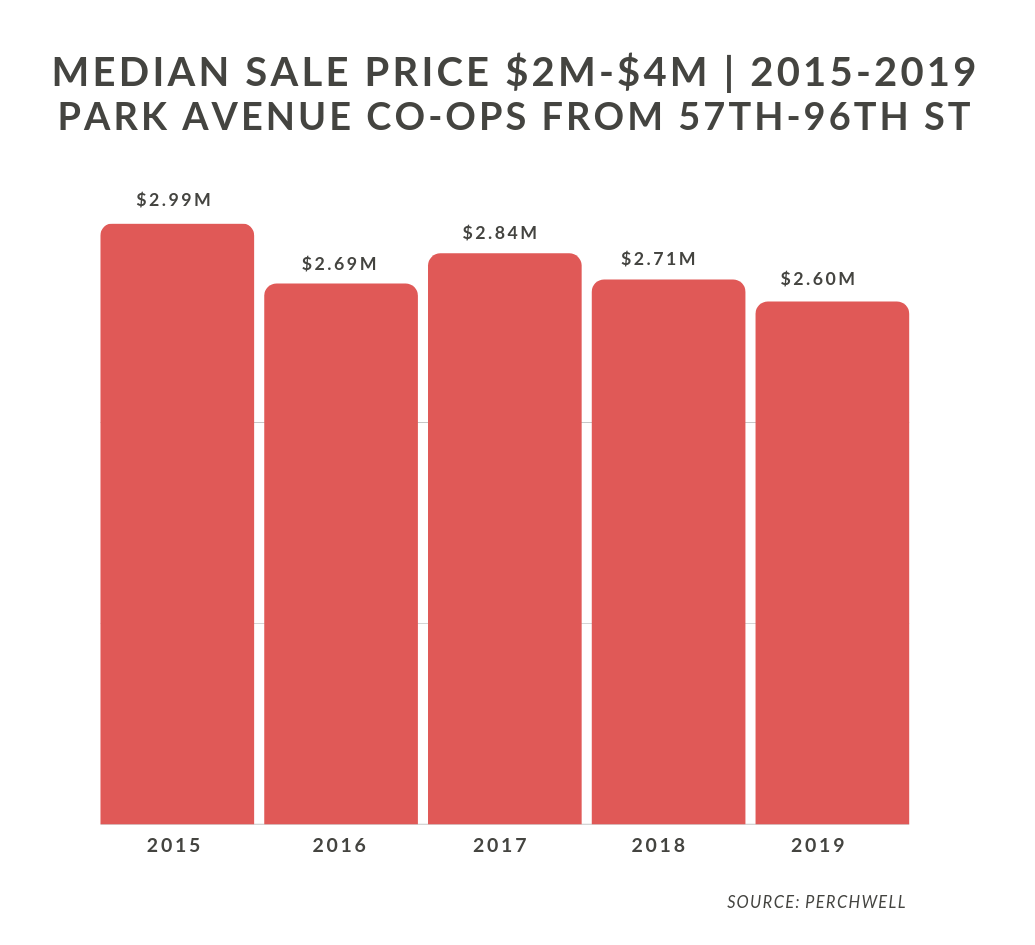

With the exception of Vornado’s project at 220 Central Park South, which pretty much sold out without negotiating prices, making concessions, marketing, or holding open houses, (who says people don’t want what they think they can’t have?) more supply still remains in the market than demand. So many three-bedroom co-op apartments on Park Avenue have been for sale that a number of those in need of renovation have recently traded for under $3 million, between 15% and 20% below where they would have sold in 2015/2016.

Unrenovated co-op units, whatever the location, require that special buyer who will both brave the co-op Board approval process and THEN brave the co-op Board renovation process. No wonder they trade at a discount, especially as more and more condominiums spring up all over town, including in the traditional co-op buyer strongholds of the Upper East and Upper West Sides. When a buyer can pay a little more and get a completely new apartment with no approvals necessary, buying into a prewar co-op can seem like more trouble than it is worth. Those buyers who believed they would always choose the detailing, plaster walls, and spacious layouts of prewar apartments, can now find high quality construction, tall ceilings, large rooms, beautiful large kitchens and baths, and full suites of amenities in new construction. And everything is new.

Overall, ongoing price capitulation and the urgency imposed by the new mansion tax costs drove greater activity in the upper market ($5 million and above), which has logged more contracts signed in June than in any of the past 12 months. With unemployment low, the stock market high, and no expectation of another increase in interest rates, the market seems poised to stabilize and even creep marginally higher during the balance of the year. That said, the local real estate market has defied prediction in the last years, leading rather than following the national downturn and now showing signs of life at a time when the national market remains in the doldrums. What’s next? We will have to wait and see.