Frederick Peters

President Emeritus

New York’s real estate market has blazed a complex path through 2017. Sales volume has remained strong, and price records have been set throughout the year in the new condominium marketplace. Most of those records have however pertained to deals signed several years earlier for buildings then under construction. For those buyers who have wanted to flip their units after closing on them, the resale market has been less kind. Prices are down anywhere from 5% to 15% across the broader market, and this has led the sellers of these newly closed super luxury condos to break even prices at best; more often, those sales have occurred at a slight loss. The rental market has been no kinder. Many of these units were bought as investments, and the flood of them reaching the rental market has reduced those values as well, sometimes as much as 20% from previously achieved rents for similar or identical units.

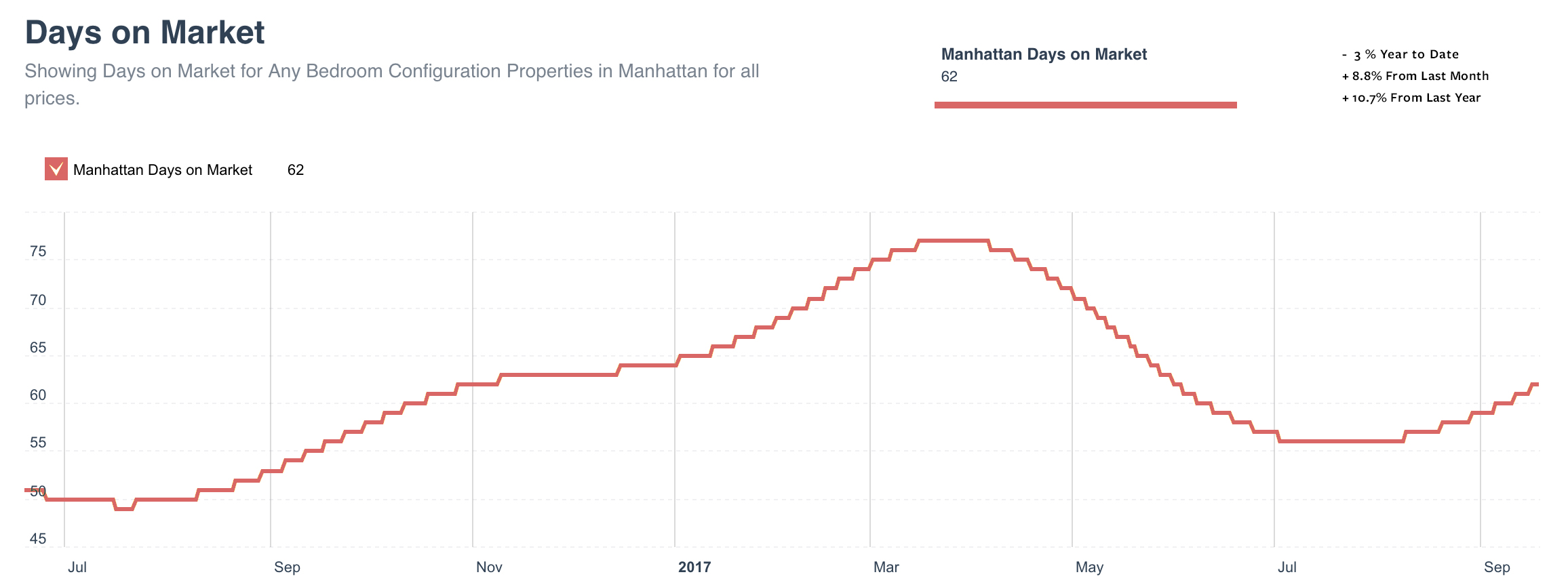

Both inventory levels and time on the market are up year over year in the third quarter. Clearly, as properties stay on the market longer, the level of listing saturation increases. Buyers become more aggressive; sellers become more anxious. Deals at negotiated prices have become the norm for all but the least expensive or most unique properties, which remain in high demand.

July and August were, as they always are, slower both in terms of inventory coming onto the market and coming off the market due to sales. But this year, the summer followed on a tepid spring market, allowing inventory to creep up further.

The summer and early fall’s most striking feature: price reductions! Hundreds come across the transom every day. This reflects two phenomena which can combine to create a bit of a storm: the market is in decline price-wise, while at the same time many sellers, reluctant to accept this fact, continue to insist on overly ambitious pricing for their properties. So properties may be priced high at the exact moment when the only genuine selling strategy is to acknowledge the downward pressure on value and price accordingly.

Sellers fear reducing prices because they don’t want to “tarnish the property.” Often when they do finally reduce, the reductions are too small to be significant. This summer we have seen this particularly in the co-op market, which continues to lag behind condos in price per foot by a margin of 15% to 20% for similar units. As I have noted before, the invasiveness of Board approval requirements combined with onerous and often costly renovation rules render the majority of co-op apartments, almost all of which need at least SOME work, far more challenging to sell. Even when agent marketing creates a steady stream of visits to the unit, fewer buyers than ever care to undertake the hassle of a co-op purchase and renovation. For those buyers who are willing, this creates real opportunity. Anyone who anticipates remaining in place for many years should absolutely be looking at co-ops. What your money will buy you, if you can tolerate Board scrutiny and managing some construction, is (in relative terms) greater than ever before.

2017 continues to be the year in which disgruntled Manhattan- and Brooklynites look north. Queens is experiencing a renaissance of formerly Manhattan-centric buyers who love its easy subway access to midtown and its multi-ethnic neighborhoods filled with great food and vibrant street life. In Manhattan, Inwood and Washington Heights are more popular than ever with young professionals, even as prices there have doubled since 2010. And gentrification is definitely coming to parts of the Bronx. Areas like the Grand Concourse, middle class in the 1940s and 1950s, became submerged in urban blight during the subsequent decades but are now re-emerging.

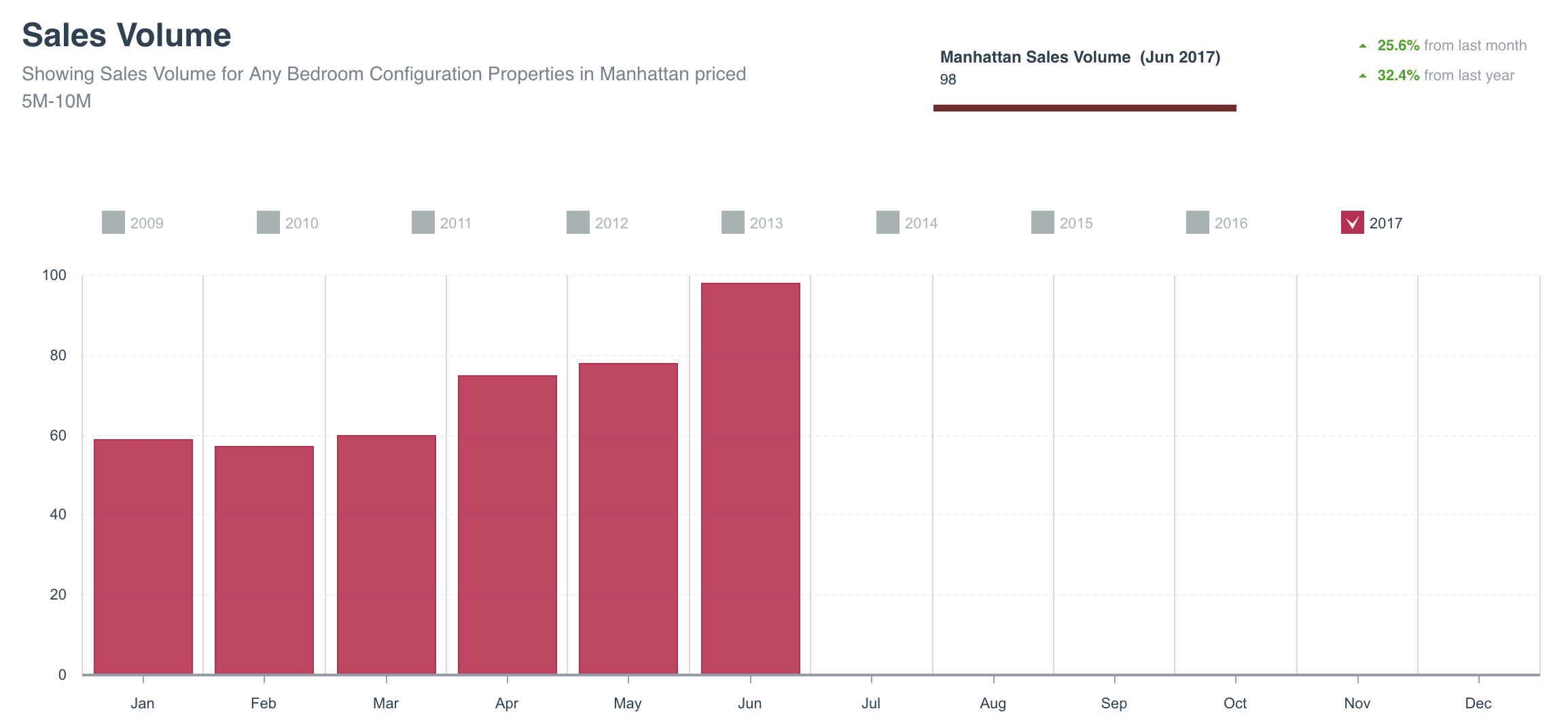

Larger deals, those at $5 million and above, have also made something of a comeback during the past 3 or 4 months. There is a bump in sales, maybe an increase in volume of 5% to 10%, which, while not rendering that market brisk, at least helps to rescue it from the doldrums it experienced during the first quarter.

We don’t anticipate big changes in the market as we move into the final quarter of the year. Inventory absorption should remain steady, and well-priced properties will continue to sell, if in two months rather than two weeks. The market will disappoint sellers with even mildly unrealistic expectations, and reward buyers who act to lock in better prices. Whenever there is a market correction, many buyers fear that they should wait longer to benefit from even lower prices; they are the ones who miss the market and only buy when prices begin to move up again. For now the market is stable: lower than a year ago but not changing much in value from week to week. It’s a good time to do business.