Frederick Peters

President Emeritus

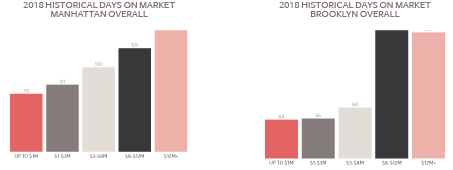

During the second quarter of 2018, New York City real estate stabilized. After a number of quarters during which both sale prices and sales numbers continued to descend, the spring brought a measure of stability to the turbulence which has characterized the market since late 2015. While supply continues to exceed demand throughout most of Manhattan (though not so much Brooklyn and Queens), sellers increasingly brought their prices into alignment with buyer expectations. As that happens, transactions materialize. That said, many properties are still experiencing multiple months on the market, and the need for price reductions, in order to trade.

The top end of the market continues to experience heavy price pressure due to inventory. As often happens at this point in the real estate cycle, projects planned when prices were peaking actually come to market at a less auspicious time. As new ultra-luxury inventory joins the many unsold units already available, downward price pressure on these units increases. Developers today negotiate substantially off asking prices and offer concessions such as paying attorney fees and transfer taxes to promote sales in these new buildings. So many cocktail parties are thrown at these various buildings that an enterprising agent could live entirely on hors d’oeuvres and champagne without ever returning home to eat!

In Manhattan, the neighborhood with the largest backlog of units remains the Upper East Side. While the market remains fairly brisk below $2 million, the larger apartments, especially co-ops in need of renovation, don’t sell easily. The continuing challenge of unrealistic Board expectations and subsequent Board rejections further devalues co-op apartments, as do onerous summer-only renovation rules. Combine this with the challenge for sellers whose sales price expectations require adjusting and you have a marketplace in which co-op inventory for two and three-bedroom apartments stands at a decade-long high.

While Brooklyn is certainly no bargain after a long and ongoing run-up in prices, it remains hot. Areas such as Windsor Terrace and Prospect-Lefferts Gardens, at the far end of Prospect Park, now see townhouse sales in the multiple millions, as do Midwood and Ditmas Park. Apartments are not any cheaper than on the Upper West Side or Carnegie Hill east of Lexington Avenue. The difference is in demand; the Brooklyn units attract bigger open house crowds and sell faster, often with multiple offers. While the Long Island City market does not quite compare, additional units are being built and quickly absorbed there as well as younger people discover the benefits of being only a subway stop or two away from 59th Street or Grand Central. And now all eyes are on Astoria!

We at Warburg have seen sales volume pick up substantially throughout May and June. While we still have our share of lingering exclusives, most inventory WILL trade once the price is right (although it can be a challenge figuring out just what that number is). Buyers remain reluctant to look at any property which they believe is incorrectly priced; we explain this time and again to sellers who ask us “Why don’t they just make an offer?” They just don’t, these days. They need to see that the seller is as committed as they are.

Going forward, I anticipate a busy summer but little price movement. I think the good economic and jobs news have halted the decline in prices, but there remains enough uncertainty in our country to inhibit any increase in prices, especially with midterm elections approaching. For now, the market, though unforgiving to ambitious sellers, seems stable.