Frederick Peters

President Emeritus

Overbids! Multiple offers! The New York City real estate market came alive in the first quarter of 2024. Transaction volume ticked up substantially across all categories, with the second week in March seeing the number of contracts executed for $4 million or more in Manhattan rising to forty, a number not seen in well over a year. Particularly interesting was the increase in large co-op sales, which accounted for eight of the twenty-five $4 million-plus contracts during March’s 3rd week. While the majority of larger sales still fall between $4 million and $10 million, there have also been a few sales in the $20 million range. This demographic, however, has slowed substantially in volume since 2021. The really big condo buyers just don’t seem to be in town these days!

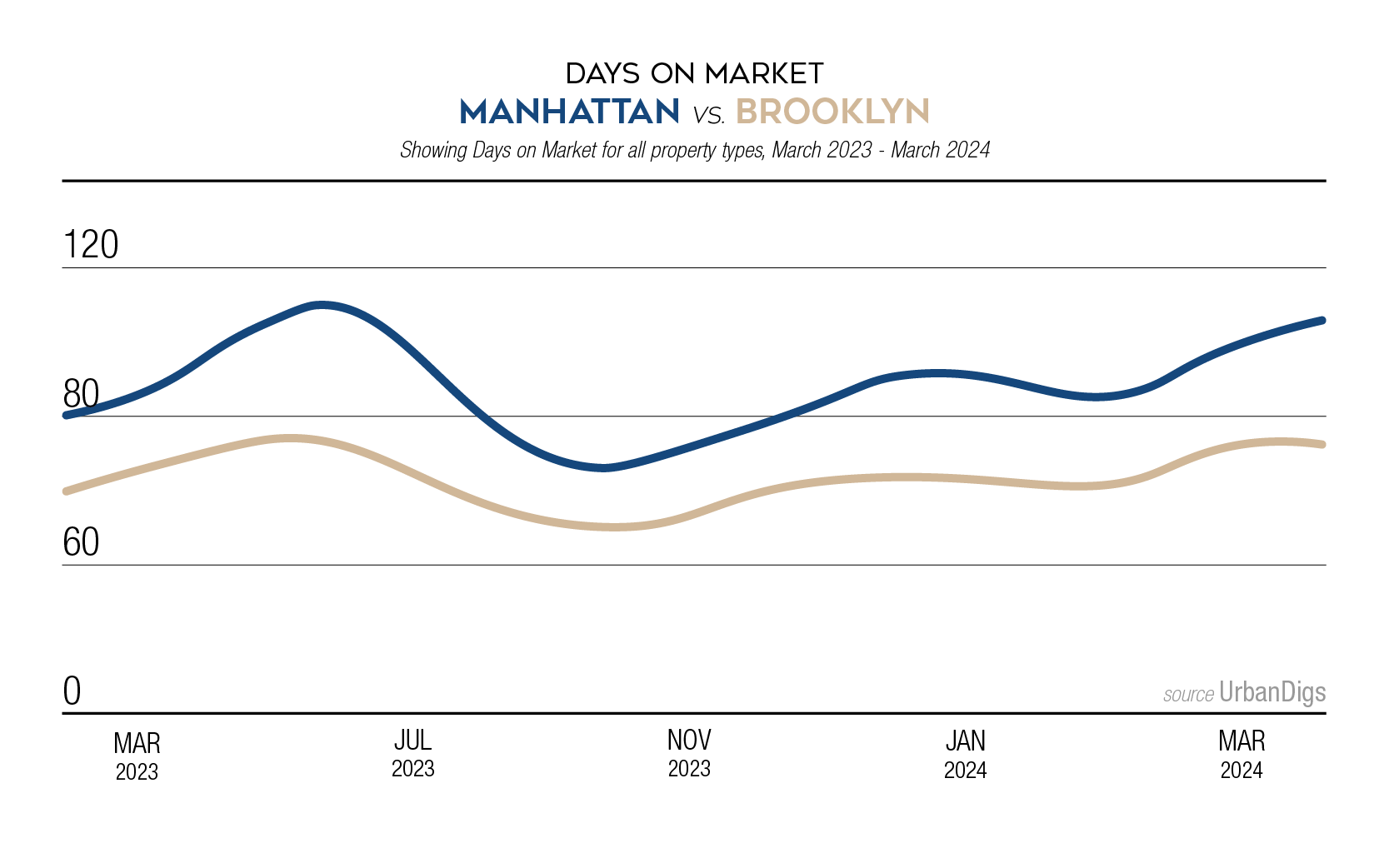

The Brooklyn market continues to run hot, although the prices for houses in the more fully gentrified neighborhoods may be approaching a tipping point as they reach $6 million, $7 million, even $10 million or more. Overall, the Brooklyn housing boom continues to move south, as even smaller houses in Prospect-Lefferts Gardens and Midwood now seem to be asking $2 million, and the elegant Victorians in Ditmas Park are approaching that threshold.

The Brooklyn market continues to run hot, although the prices for houses in the more fully gentrified neighborhoods may be approaching a tipping point as they reach $6 million, $7 million, even $10 million or more. Overall, the Brooklyn housing boom continues to move south, as even smaller houses in Prospect-Lefferts Gardens and Midwood now seem to be asking $2 million, and the elegant Victorians in Ditmas Park are approaching that threshold.

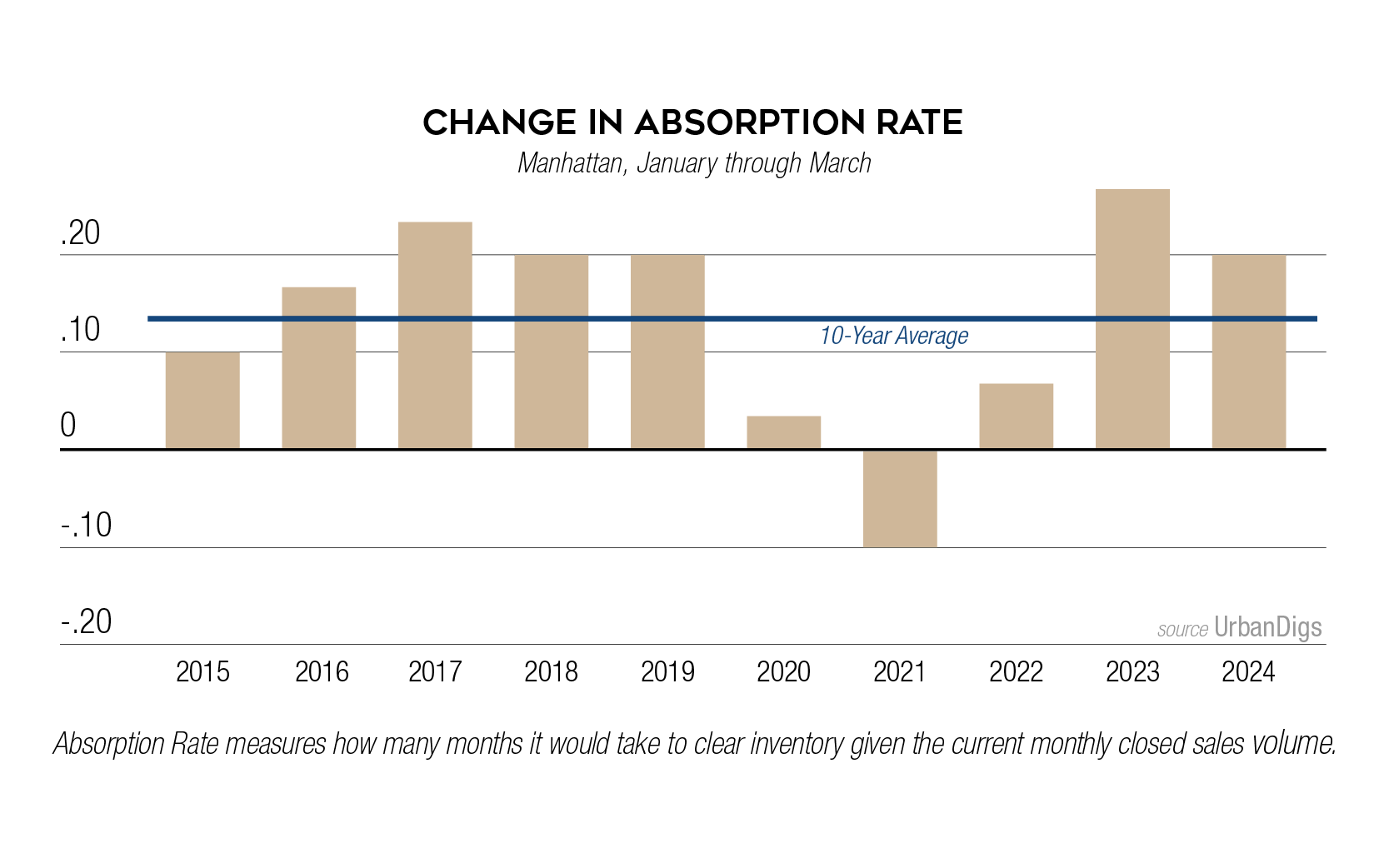

Multiple bids and overbids have also returned to the market, especially where properties are properly priced. While many larger units priced above $10 million remain for months and even years on the market because of unrealistic pricing, others are trading in thirty days or less with two or even three competing offers. There have been exceptions, but these properties are mostly in good condition and well-priced for the value they provide. In 2014 and 2015, buyers overpaid because the market was rising so fast they were confident the market would catch up to their price between the contract and the closing. Those days are long gone. Buyers are active again, having made their peace with interest rates, but the market shows no signs of exuberance.

Condition remains a make-or-break issue in the minds of most buyers. Supply chain issues continue to weigh on access to renovation materials, and homeowners continue to renovate rather than move so as to hang onto their cheap mortgages. In this environment, today’s buyers are reluctant to undertake the time and expense involved in upgrading dated properties. Throughout all price ranges, properties in poor condition remain the toughest sell. Many buyers won’t even look at them, and even when they do, they tend to react with the phrase, “Too much work.” Aggressive price incentives provide the only possible route to a reasonably quick sale for these units.

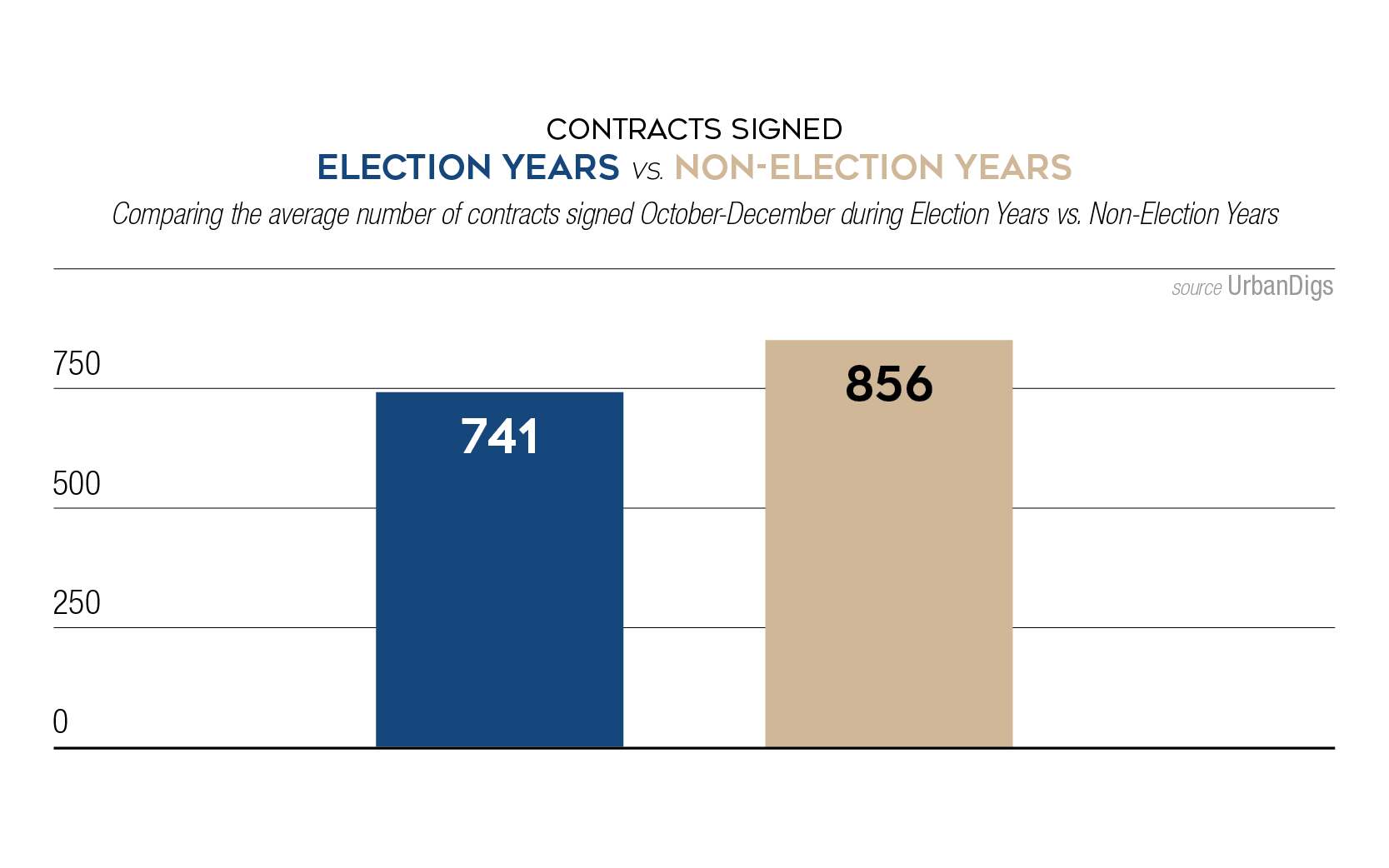

In the middle of the quarter, the National Association of Realtors settled its part of the class action lawsuit regarding the payment of buyer-side commissions. Most of the major brokerages had settled months before. While this settlement has excited a flurry of attention from the press, the ramifications for New York City are likely to be minimal. Our commissions have always been negotiable. Our listing service never required the inclusion of buyer-side commissions. And most of our clients and customers understand that our system has always provided balanced representation on both sides of the transaction. Higher interest rates have not held back the national economy, which has continued to add jobs every month, or the stock market, which has continued to rise throughout the quarter. Even if the latter cools, the recession, soft or hard, which so many economists have predicted from one quarter to the next has not arrived. The most significant blip on the horizon is the Presidential election, which always slows market activity in the latter part of the year. But the spring selling season has opened strong and looks to continue that way. More inventory will hit the market in April, and as long as it is priced right, buyers will be waiting there to scoop it up. New Yorkers, no matter the other issues, have always had a limited tolerance for delayed gratification.

Higher interest rates have not held back the national economy, which has continued to add jobs every month, or the stock market, which has continued to rise throughout the quarter. Even if the latter cools, the recession, soft or hard, which so many economists have predicted from one quarter to the next has not arrived. The most significant blip on the horizon is the Presidential election, which always slows market activity in the latter part of the year. But the spring selling season has opened strong and looks to continue that way. More inventory will hit the market in April, and as long as it is priced right, buyers will be waiting there to scoop it up. New Yorkers, no matter the other issues, have always had a limited tolerance for delayed gratification.